FlexiPe BNPL App Development

How Solguruz helped launch a BNPL solution that enables users to shop, pay bills, and split payments with ease.

FlexiPe is a Buy Now Pay Later (BNPL) app built by SolGuruz for a US-based fintech in 8-10 months. The product runs on native iOS and Android apps, a Python-powered web app, and a Python backend with OAuth 2.0, AWS firewall rules, and automated rollback, with WordPress driving the marketing layer. It lets users split retail purchases and utility bill payments into scheduled installments, combining shop-now BNPL with bill-pay flexibility in a single product.

Buy Now, Pay Later

Payments have never been easier

Buy Now, Pay Later

Project Snapshot

Industry

Finance / FinTech

Platforms

Web (WordPress) + Native iOS + Native Android

Timeline

8-10 months (concept to production launch)

Client Location

Oakland, California, USA

Key Differentiator

Combined retail BNPL + utility bill installment flow in a single app

Project Overview

The client is a US-based fintech headquartered in Oakland, California, planning to enter the Buy Now Pay Later market with a differentiated product, one that combines retail installment payments with a bill-pay use case. The goal: help consumers split checkout purchases and utility bills into scheduled installments, approve them in real time, and settle with merchants or billers instantly.

SolGuruz delivered FlexiPe in 8-10 months. The product spans a native iOS app, a native Android app, and a WordPress-based web surface, backed by a Python API layer and AWS infrastructure with PCI-DSS-aligned security practices. Every decision was made against the realities of 2026 BNPL regulation, CFPB Reg Z in the US, state money transmitter laws, and KYC/AML requirements.

This case study walks through the problem, the solution, the full development process, the tech stack, the UI design, compliance practices, and the 2026 competitive landscape.

What Is a Buy Now Pay Later (BNPL) App?

What BNPL Means

A Buy Now Pay Later (BNPL) app is a mobile or web application that lets users split retail purchases or bill payments into scheduled installments, typically 3 to 6 payments spread across 6 weeks to 12 months. BNPL apps sit between consumers and merchants as a short-term credit layer, handling credit decisioning, payment scheduling, merchant settlement, and repayment collection.

FlexiPe in Context

Leading BNPL apps in 2026 include Klarna, Afterpay, Affirm, Zip, and PayPal Pay Later globally, alongside regional players like Simpl and LazyPay in South Asia. FlexiPe was built to compete in this category with a differentiated focus on utility bill installment payments alongside traditional retail checkout BNPL.

Overview of Buy Now Pay Later

History & Evolution

The modern BNPL model traces to Klarna, founded in Sweden in 2005, followed by Affirm in the US in 2012 and Afterpay in Australia in 2014. The concept itself is older than department store layaway plans in the early 1900s, which operated on similar principles. Digital BNPL scaled globally during the 2020-2022 e-commerce boom.

Regulatory Framework 2026

In 2026, BNPL operates under a maturing regulatory framework: the CFPB’s May 2024 interim final rule treats US BNPL lenders as credit card providers under Regulation Z, the UK FCA has moved on to statutory BNPL regulation, and India’s RBI Digital Lending Guidelines apply to BNPL operators in that market.

How Does a BNPL App Work?

Every BNPL transaction follows a five-stage flow. Understanding this architecture is essential to building, evaluating, or scoping a BNPL product:

Merchant Integration

The BNPL option appears at merchant checkout via an API integration, SDK, or hosted checkout page. Modern BNPL apps embed with 2-3 lines of code for e-commerce platforms like Shopify, WooCommerce, and Magento.

Credit Decisioning

When a user selects BNPL at checkout, the app runs a real-time credit check using bureau APIs (Experian, TransUnion, Equifax) or proprietary scoring models that combine alternative data like bank transaction history, prior BNPL repayments, and device signals. Decisioning completes in 2-4 seconds.

Approval and Disbursement

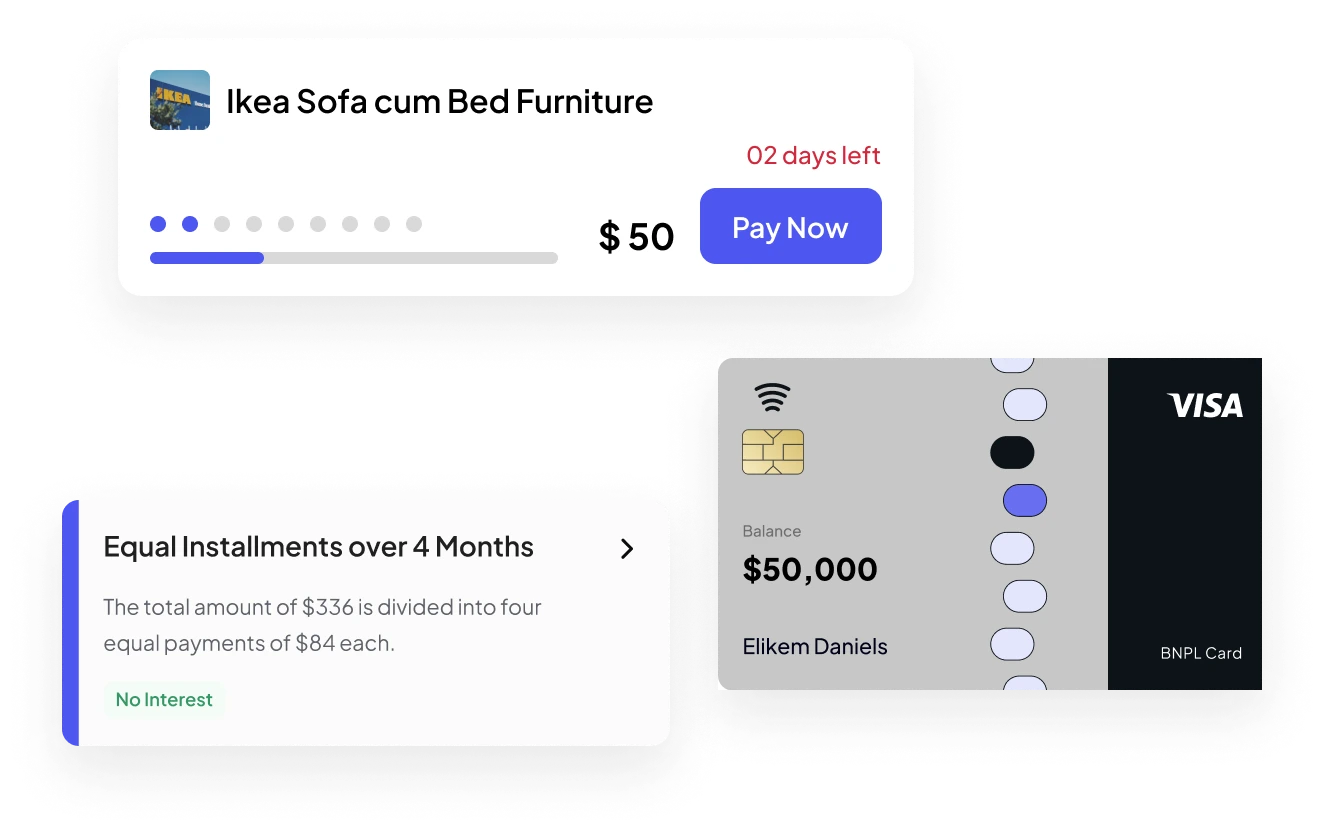

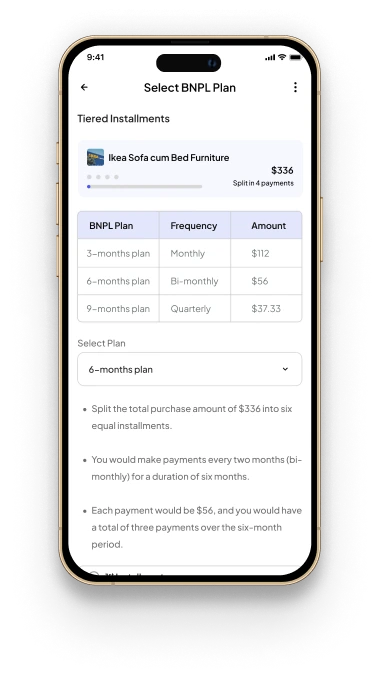

On approval, the merchant is paid in full immediately by the BNPL provider. The consumer receives an installment schedule, commonly 4 equal payments over 6 weeks (Pay-in-4) or monthly installments for larger purchases.

Installment Collection

The app auto-debits each installment from a linked payment method (card or bank account) on scheduled dates. Failed payments trigger retry logic, late fees (where legally allowed), and structured communication flows.

Reporting and Compliance

Repayment behavior is logged for internal scoring and, where applicable, reported to credit bureaus. Under CFPB Reg Z in the US, BNPL lenders must now provide consumer protections similar to credit cards, including dispute resolution and refund handling.

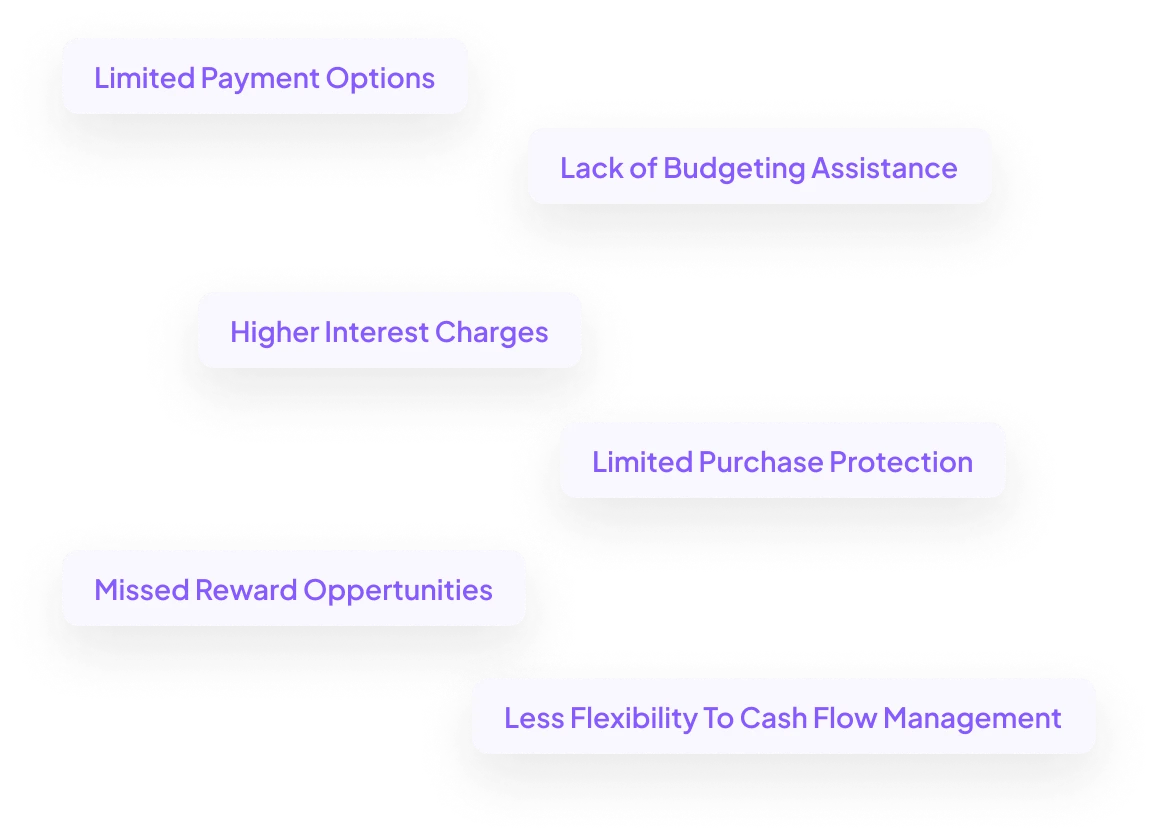

Why Did the Client Need a BNPL App?

Buy Now Pay Later applications are one of the fastest-growing FinTech services, enabling customers to split the cost of retail goods or services into specific installments, with the first payment due upfront. The US BNPL market alone processes hundreds of billions of dollars annually in 2026, with continued growth driven by regulatory clarity and consumer demand for flexible credit.

The client saw three specific market gaps:

Most BNPL apps handle retail checkout only. Utility bill installment payments are an underserved vertical, especially for lower-income segments managing cash flow around payday cycles.

Bill-pay BNPL requires different credit modeling than retail BNPL - bills are recurring, which changes the risk profile and scoring approach.

Integrated retail + bill-pay BNPL creates a single trusted consumer app for financial flexibility, reducing churn across both use cases.

The client wanted to enter the FinTech market with a differentiated BNPL application that could serve both retail and bill-pay with the flexibility modern consumers expect.

Credit decisioning, merchant settlement, and multi-state compliance - we handle the full stack. Share your scope and get a build plan in 72 hours.

What BNPL Solution Did SolGuruz Build?

SolGuruz mobile and web development team built a production-grade BNPL platform with a user-centered design and data security as the top architectural priority. The solution delivered:

Native iOS and Android apps with checkout, bill-pay, payment scheduling, and account management

A Python-powered web app for credit onboarding, KYC document upload, and dispute handling

Python backend APIs handling credit decisioning, merchant settlement, installment scheduling, and reporting

AWS infrastructure with PCI-DSS-aligned security, automated backups, OAuth 2.0 authentication, and rollback capability

WordPress-driven marketing CMS for merchant onboarding content and customer education

SolGuruz Development Process - From Research to Post-Launch

FlexiPe was delivered using SolGuruz standard 10-stage lifecycle for product development. Each stage has a fixed duration, a named deliverable, and a defined team - no undefined work, no scope drift. Compliance checkpoints are woven into the architecture, QA, and deployment stages rather than treated as a separate phase.

Discovery & Market Research

Founder interviews, customer persona mapping for retail and bill-pay segments, and competitor teardowns across Klarna, Afterpay, Affirm, Zip, and PayPal Pay Later. Regulatory landscape scoped for US federal, state, and credit bureau reporting requirements.

Requirements & Scope Finalization

User stories and acceptance criteria written in Gherkin format for every feature. Data flow diagrams for credit decisioning, merchant settlement, and installment collection. Scope locked with explicit carve-outs.

UI/UX Design

Figma-based design system covering native mobile apps, the Python web app, and merchant-facing touchpoints. Checkout flow optimized for sub-8-second completion. 15 usability tests run before developer handoff.

Architecture & Technical Planning

System design covering credit decisioning pipeline, merchant settlement flows, installment scheduling. Database schema modeled for transaction immutability and audit readiness. Security threat modeling against OWASP Top 10 and fintech-specific vectors.

Mobile App Development

Native iOS and Android builds of the consumer mobile app. Core flows: onboarding and KYC, merchant browsing, bill-pay selection, checkout integration, installment schedule view, payment method management, and notifications. Offline-first handling baked into each platform.

Backend + Web App Development

Python-powered web app handling credit history, KYC document upload, dispute resolution, and account management. Python backend for credit decisioning API calls, merchant settlement, and installment scheduling. WordPress headless CMS for marketing content.

Quality Assurance & Testing

Functional testing across 20+ device profiles covering iOS, Android, and responsive web. Independent penetration testing. Load testing at 2-3x projected launch volume. Full transaction flow testing in staging. PCI-DSS readiness review and KYC/AML flow sign-off.

Deployment

App Store and Play Store submission with fintech-specific metadata. Web app deployed to AWS production. Firewall rules locked, database backup policies verified, monitoring dashboards activated. Soft launch in limited US state footprint.

Post-Launch Support & Maintenance

Dedicated support team for post-launch. Crash monitoring, payment failure rates, credit decision latency, and fraud indicators tracked continuously. SLA: critical bugs within 24 hours, high-priority within 72 hours.

Iteration & Feature Evolution

Post-launch evolution runs on 2-week sprints. A/B testing on checkout variants, merchant onboarding improvements, credit model refinement based on real repayment data. Quarterly regulatory reviews.

The team that built FlexiPe is ready for your fintech product. Book a 30-minute scoping call with our BNPL product lead - no decks, just scope.

Typography & Colour Palette

We have considered the below-mentioned fonts and colors for designing the FlexiPe BNPL application.

UI Design

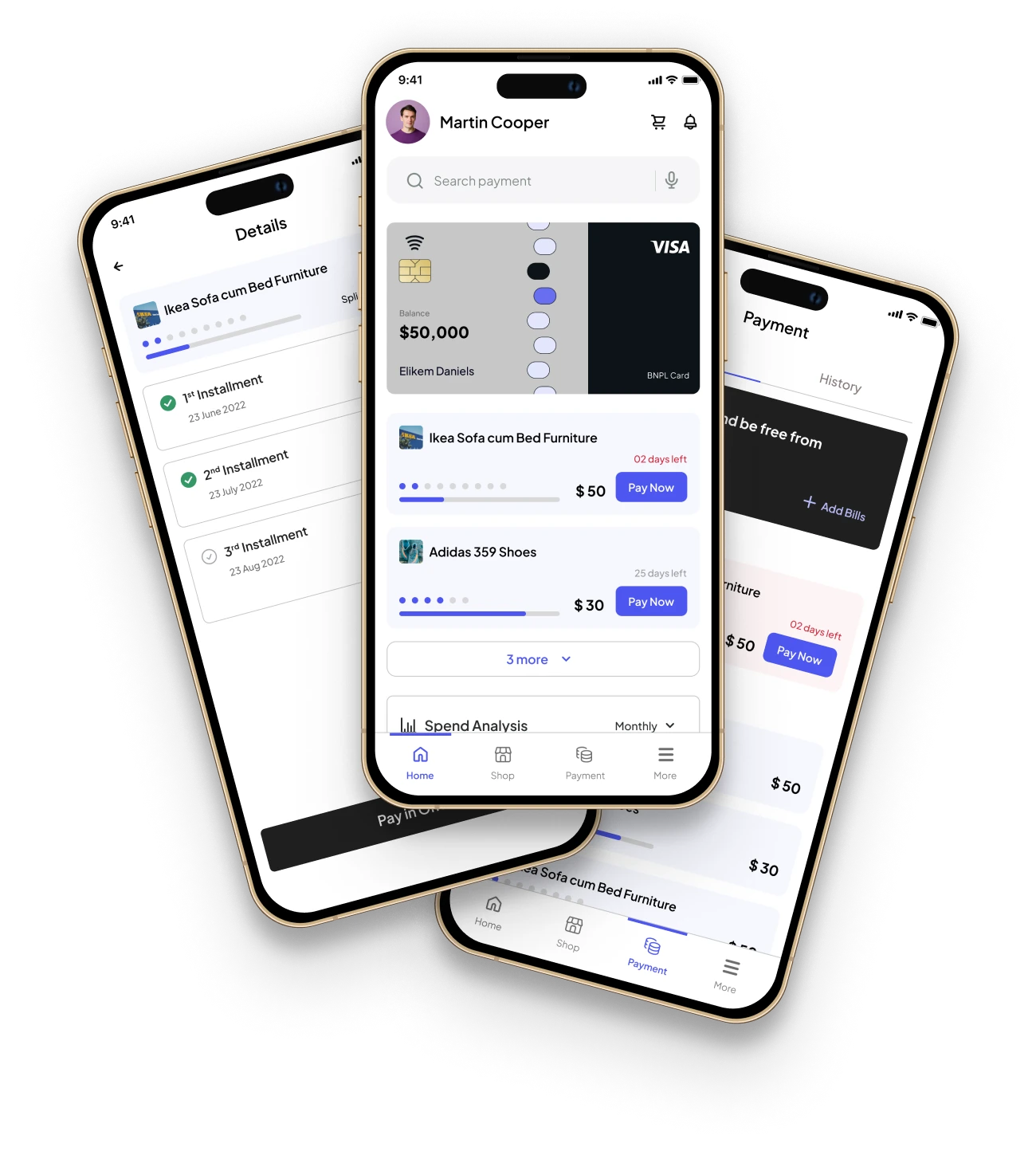

FlexiPe's UI was designed to minimize checkout friction and give users clear visibility into their payment schedules - two of the most cited UX differentiators for BNPL apps in 2026.

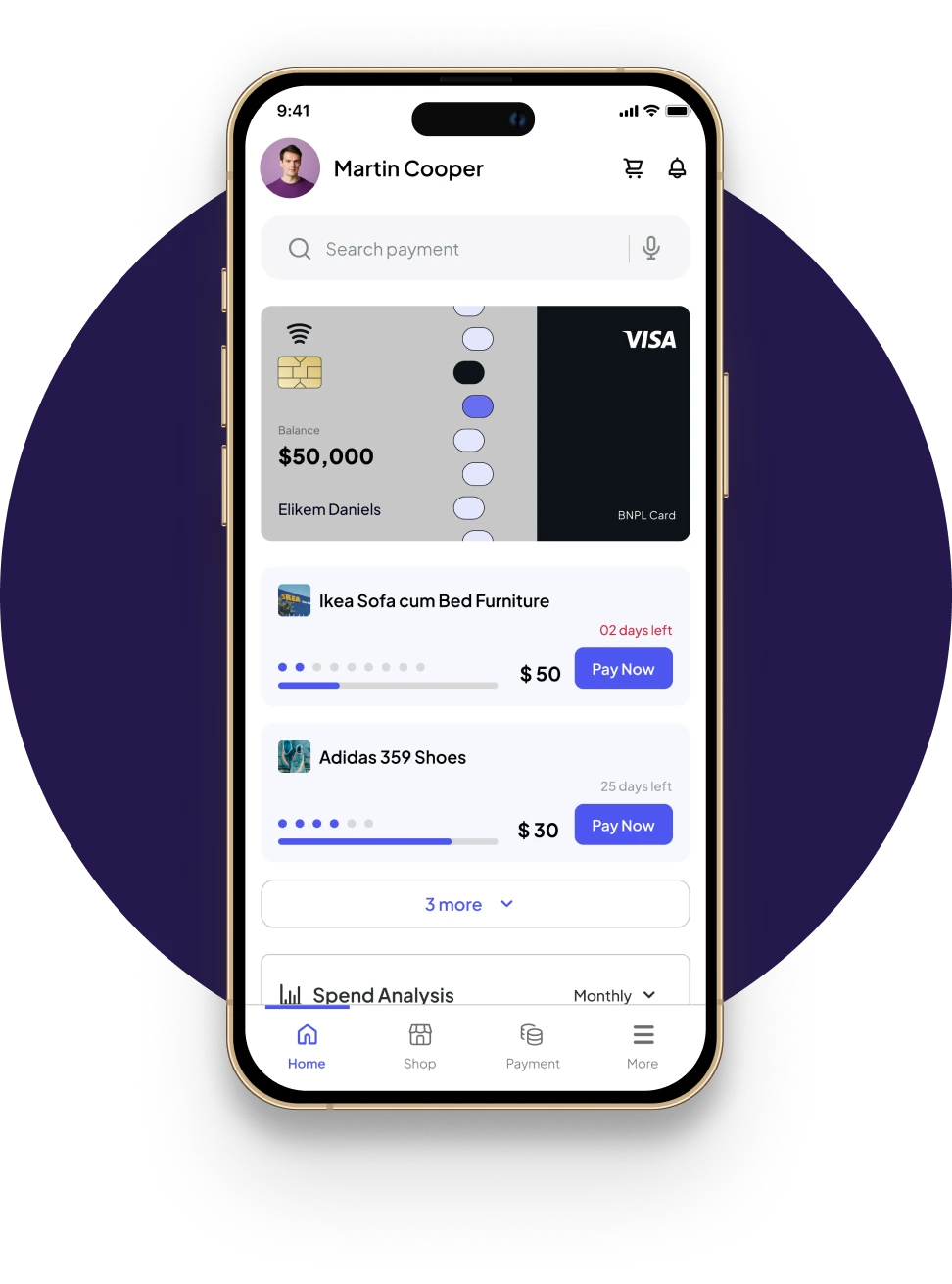

Home Screen

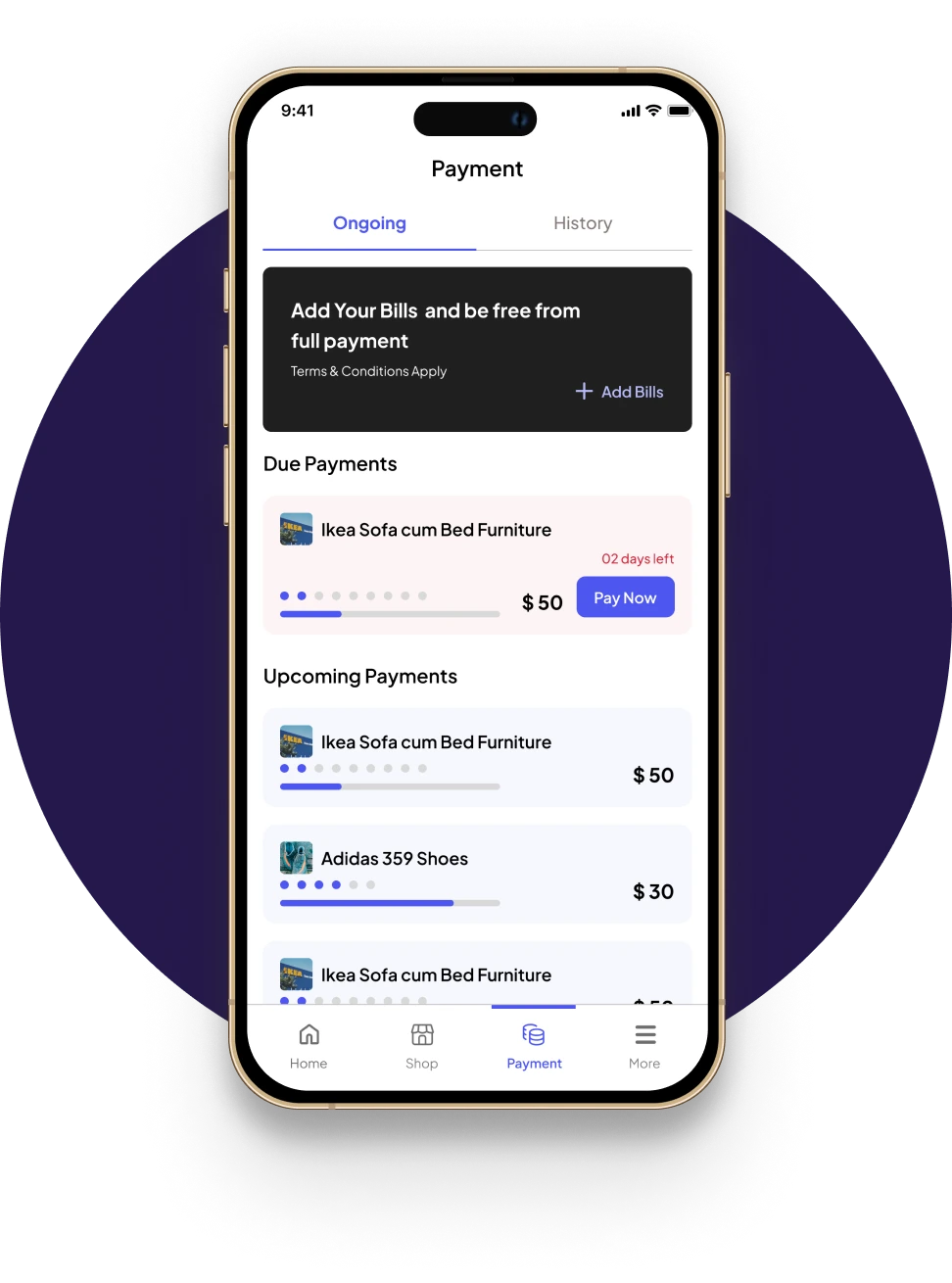

The intuitive home screen surfaces the latest due payments with a clear pay-now button, payment search options, spend analysis, and personalized recommendations. Users can see their next payment at a glance without opening any submenus.

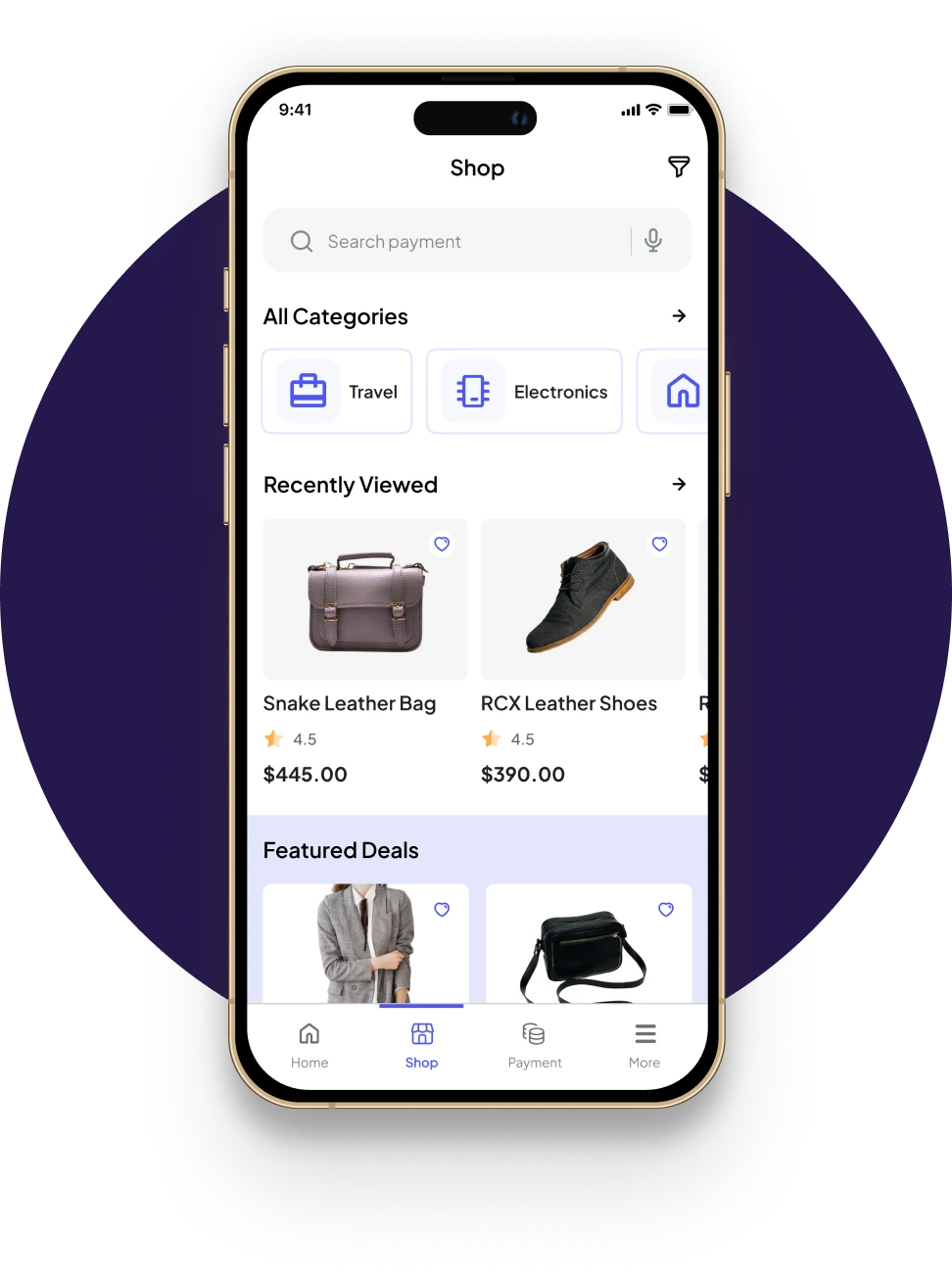

Shop Screen

The shop screen displays a curated selection of integrated merchants with recently viewed products and featured deals, designed for fast browsing and frictionless navigation into merchant-hosted checkout flows.

Payment Screen

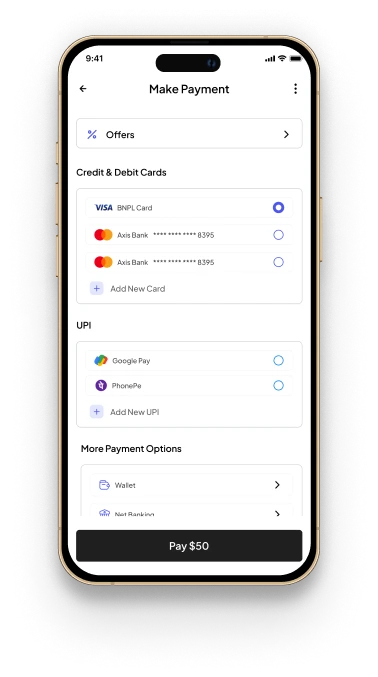

The payment screen shows the due payments list, upcoming installments, and a prominent pay-now button to clear dues on time. Late-payment warnings and fee previews appear inline to keep the financial impact transparent.

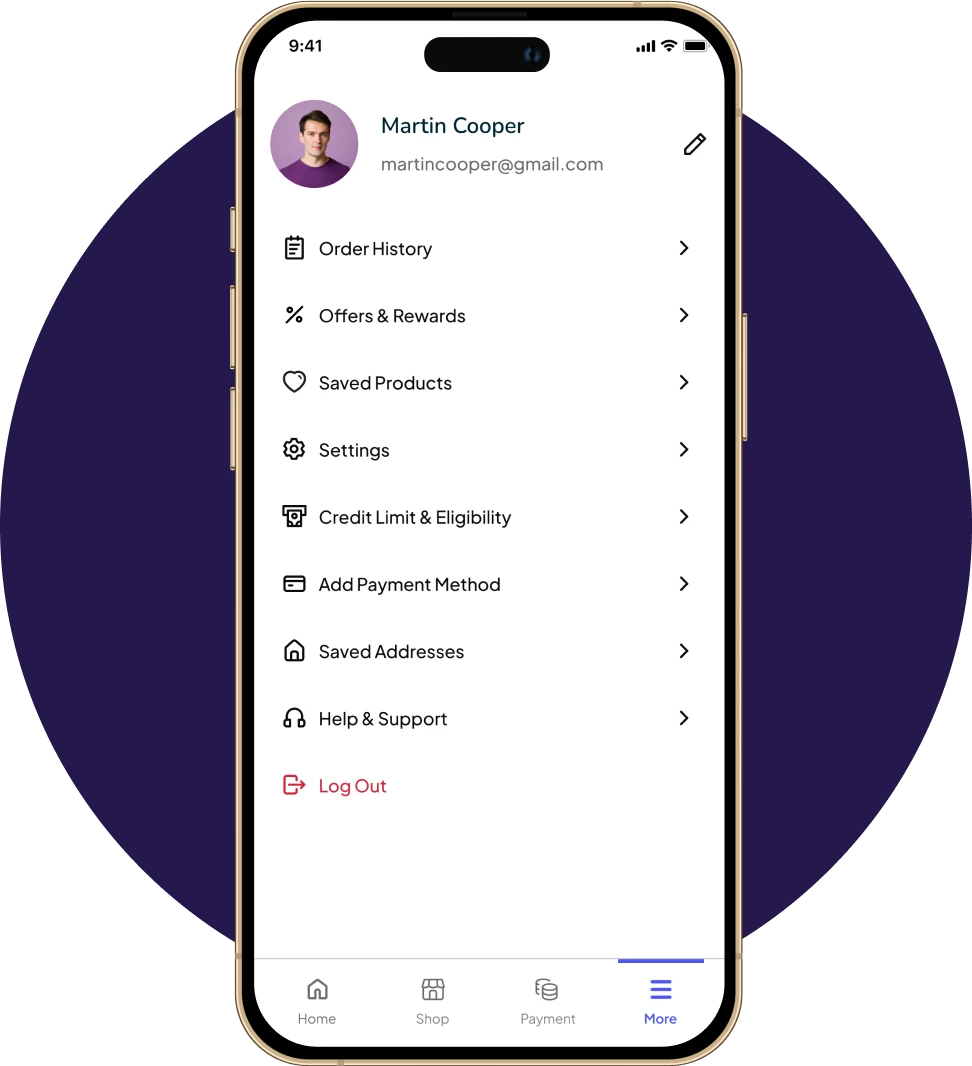

More Options (Account Menu)

The account menu includes profile editing, order history, offers and rewards, saved products, settings, credit limit and eligibility, payment method management, address management, help and support, and logout.

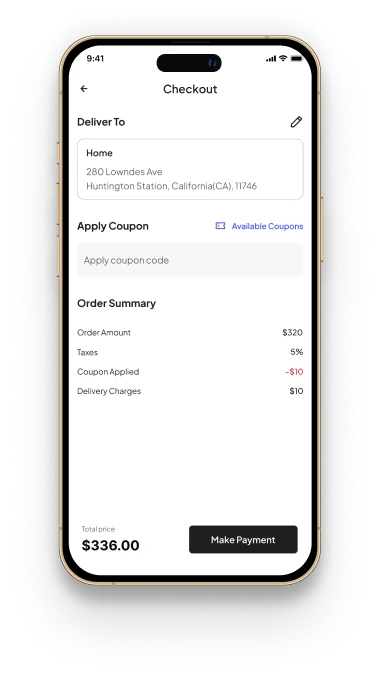

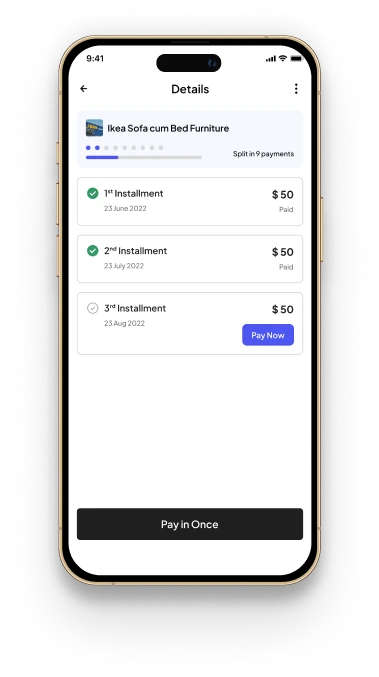

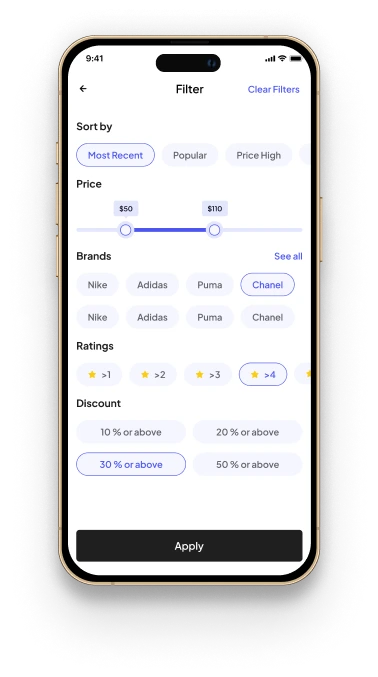

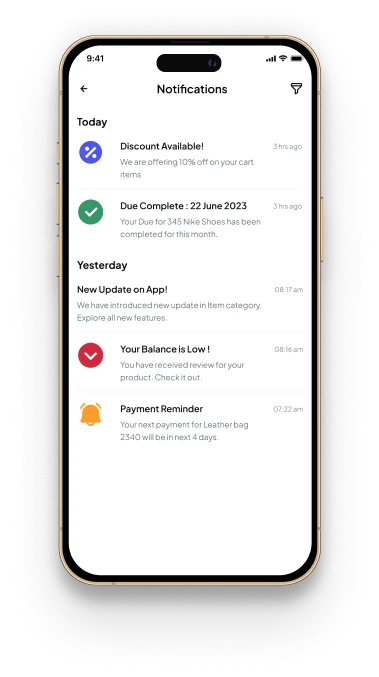

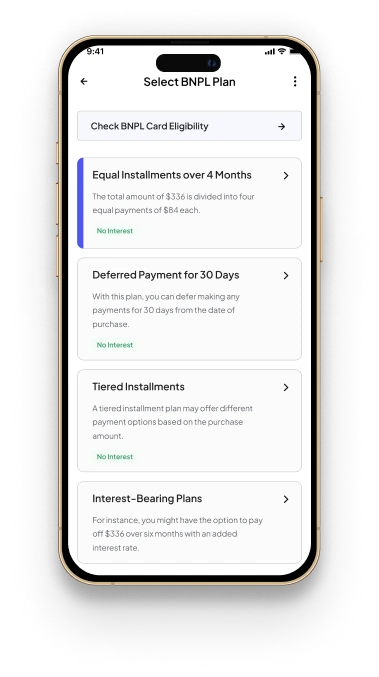

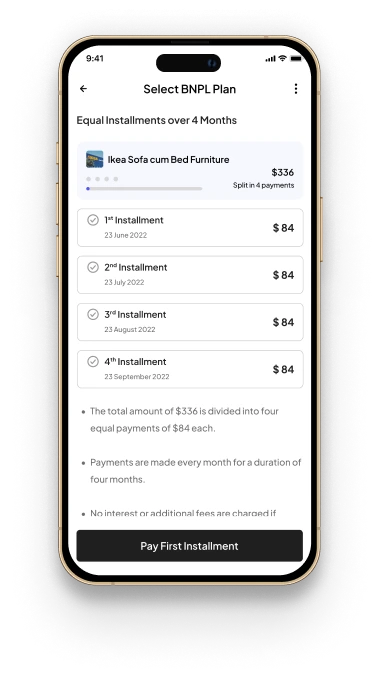

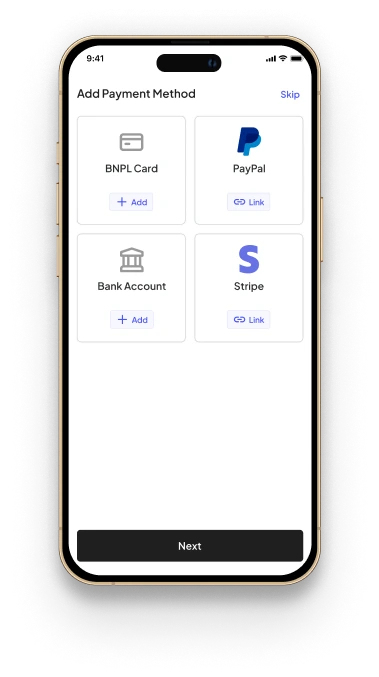

More Screens

Additional screens delivered in the app include checkout, product details, filters, payment flow, notifications, BNPL plan selection, bill-type selection, add payment method, and plan overview. Design consistency and navigation flow were prioritized across every screen.

BNPL Compliance & Regulatory Framework

BNPL is a regulated financial service in every major market. FlexiPe was built against current 2026 compliance requirements.

PCI-DSS Level 1

Any app handling payment card data must comply with Payment Card Industry Data Security Standard (PCI-DSS). FlexiPe follows Level 1 practices - the strictest tier with segmented cardholder data environments and annual audit readiness.

KYC and AML

Know Your Customer (KYC) verification and Anti-Money Laundering (AML) monitoring are non-negotiable. FlexiPe integrates identity verification providers for document + biometric checks and runs transaction monitoring for AML red flags.

CFPB Regulation Z (US)

The Consumer Financial Protection Bureau's May 2024 interim final rule treats BNPL providers as credit card lenders under Regulation Z. FlexiPe implements the required disclosures, dispute handling, and billing error resolution.

State Money Transmitter Licensing

US BNPL operators must hold money transmitter licenses in states that require them. FlexiPe's launch plan included state-by-state compliance verification before activating service in each jurisdiction.

GDPR (EU Users)

For any EU users, FlexiPe follows GDPR data handling standards, consent capture, data portability, right to erasure, and breach notification within 72 hours.

SolGuruz Security & Compliance Credentials

SolGuruz is ISO 27001:2022 and ISO 9001:2015 certified, with security practices audited against both standards, which meet or exceed the security posture expected for fintech product delivery.

Buy Now Pay Later Apps: Competitive Analysis

The BNPL market in 2026 is dominated by five global players plus a long tail of regional competitors. Here is how FlexiPe is positioned:

App

Market Position

Core Strength

Gap or Limitation

Market Position

Global Market Leadership

Sweden-founded, now operating in 45+ countries

Core Strength

Comprehensive Merchant & Product Ecosystem

Deep merchant network, Pay-in-4 and longer financing options, integrated shopping app

Gap or Limitation

Fee Complexity & Multi-Market Regulatory Burden

Complex fee structures across merchants; regulatory scrutiny in multiple markets

Market Position

Block-Backed with Regional Strength

Owned by Block (Cash App); strong US + Australia presence

Core Strength

Gen-Z Appeal & Ecosystem Integration

Zero-interest Pay-in-4, strong Gen-Z brand positioning, tight Cash App integration

Gap or Limitation

Limited Financing Depth & Regulatory Pressure

Limited long-term financing options; late-fee revenue model under regulatory pressure

Market Position

Public Market Leader with Flexible Terms

Publicly listed US leader; 0-36 month installment options

Core Strength

Transparent Pricing & Top-Tier Partnerships

Transparent no-hidden-fee pricing; deep Shopify and Amazon partnerships

Gap or Limitation

Higher Cost & Checkout Friction

Higher interest rates for longer loans; added credit-check friction at checkout

Market Position

Regional Specialist Player

Australia-founded; US and ANZ market focus

Core Strength

Unified Two-Tier Product Strategy

Zip Pay (4-installment) and Zip Money (longer financing) under one brand

Gap or Limitation

Limited Scale Outside Core Markets

Smaller merchant network outside core markets; ongoing profitability pressure

Market Position

Ecosystem-Embedded Global Reach

Embedded in PayPal's existing US + global base

Core Strength

Frictionless Approval via Existing Data

Instant approval leveraging PayPal account data; no new account needed

Gap or Limitation

Weak Standalone Identity & Platform Dependency

Limited standalone product identity; dependency on PayPal checkout

Security Practices Implemented

Multiple layers of security were implemented across network, data, cloud, application, and endpoint levels, each essential for a fintech app handling payment credentials and consumer credit data.

Data Encryption

Data is encrypted in transit and at rest. Transport uses HTTPS with TLS certificates. Storage uses full-disk encryption on database instances plus field-level encryption for payment and PII data.

OAuth 2.0 Authentication

OAuth 2.0 governs authentication flows, preventing unauthorized access and ensuring the system is only reachable by authenticated users. Scope-based permissions limit what each token can access.

AWS Firewall Rules

Firewalls are configured on AWS instances and databases with allow-listed services. Inbound access is restricted to essential ports, and admin access requires role-based permissions with multi-factor authentication.

Source Code Obfuscation

Source-code obfuscation is applied to release builds so the distributed binary is difficult to tamper with or reverse-engineer. Sensitive keys are stored in AWS Secrets Manager and never bundled with the app.

Automated Backup and Rollback

Cloud instances take scheduled backups at regular intervals. Rollback to a specific version is automated - recovery from a bad deployment takes minutes, not hours, which is critical in fintech where transaction integrity must be preserved.

Project Outcome

SolGuruz delivered FlexiPe across an 8-10 month build, with compliance, security, and cross-platform UX shipped as one integrated product. Each card below restates a result you can verify against the case study sections above.

Production launch in 8-10 months

From concept to live US-market product without scope drift. The 10-stage delivery lifecycle wove compliance checkpoints into architecture, QA, and deployment phases rather than treating them as a separate gate.

Compliant by design, not by retrofit

Launched with PCI-DSS Level 1 architecture, KYC/AML monitoring, CFPB Regulation Z disclosures, and state money transmitter law coverage embedded from the first sprint. Passed pre-launch security review with no compliance gaps.

One product across multiple runtimes

Native iOS and Android apps, a Python web app, and a Python API layer shipped as a single cohesive product. AWS-backed infrastructure with OAuth 2.0, automated backups, and rollback capability ready from launch.

A differentiated BNPL product

Combined retail installment payments and utility bill installments in a single app - a rare combo in the 2026 BNPL market dominated by retail-only competitors. Strategic UX/UI drove end-user engagement from day one.

Planning Your Own BNPL App?

BNPL App Development Services

Hire the team that built FlexiPe to design, build, and ship your BNPL product.

BNPL App Development Guide

The full how-to: features, the credit engine, compliance, tech stack, and cost.

Fintech Software Development

Our broader fintech capabilities across lending, wealth, insurance, and payments.

Frequently Asked Questions

Quick answers to the questions our clients and prospects ask most. If yours is not here, our team is one click away.

Need advice tailored to your project?

FAQs cover the common ground. For decisions specific to your tech stack, timeline, and team, talk directly to a senior engineer who has shipped what you are planning.

A BNPL app is a mobile or web application that lets users split retail purchases or bill payments into scheduled installments, typically 3 to 6 payments across 6 weeks to 12 months. BNPL apps act as a short-term credit layer between consumers and merchants, handling credit decisioning, payment scheduling, and settlement.

A BNPL transaction runs in five stages: merchant integration at checkout, real-time credit decisioning, approval with merchant payout, auto-debit installment collection, and compliance reporting. The full flow completes in 2-4 seconds at checkout, with installments drawn on scheduled dates afterward.

An MVP costs $60,000-$120,000 for a 3-4 month build with basic credit check and limited merchants. Standard builds with multi-merchant support, credit bureau integration, and PCI-DSS-aligned security range $120,000-$250,000 over 6-10 months. Enterprise-grade BNPL platforms reach $500,000+ across 10-16 months.

A production-grade BNPL app takes 8-10 months responsibly. Compressed timelines skip KYC, AML, and credit-decisioning infrastructure - shortcuts that surface as regulatory fines or blocked rollouts post-launch.

Native iOS and Android apps, Python frameworks for the web app (KYC, dispute handling) and backend, WordPress for the marketing/content layer, PostgreSQL for transaction-grade data integrity, and AWS for PCI-DSS-aligned infrastructure. OAuth 2.0 handles authentication. This stack balances speed, auditability, and fintech-grade scalability.

Modern BNPL was pioneered by Klarna, founded in Sweden in 2005. Affirm launched in the US in 2012, and Afterpay launched in Australia in 2014. The concept itself is older - early 1900s department store layaway programs operated on similar installment principles.

Yes. In the US, the CFPB's May 2024 interim final rule treats BNPL providers as credit card lenders under Regulation Z. The UK FCA is moving on statutory BNPL regulation. The EU applies consumer credit rules plus GDPR. India's RBI Digital Lending Guidelines apply to BNPL operators in that market.

The global leaders are Klarna (Swedish, widest merchant network), Afterpay (US and Australia, owned by Block), Affirm (US, longest financing options), Zip (ANZ and US), and PayPal Pay Later (embedded in PayPal checkout). Regional players include Simpl and LazyPay in South Asia.

PCI-DSS Level 1 for payment card data, KYC and AML monitoring for onboarding and transactions, CFPB Regulation Z for US consumer disclosures, state money transmitter licenses, and GDPR for EU users. Missing any of these exposes the operator to fines or shutdown orders.

Avoid regulatory surprises. Share your target markets and merchant plan - we’ll deliver a clear estimate, team structure, and compliance roadmap in 72 hours.

Related Projects

More Projects We Have Delivered

SolGuruz has shipped 102+ products across 14 industries. See other fintech and B2B app projects our team has delivered alongside this BNPL platform - marketplace apps and CRM portals built with the same financial product thinking and enterprise-grade reliability.

Online B2B Diamond Selling Mobile App Solution

Explore a B2B Diamond Selling App Development case study. Discover how we delivered innovative features, enhanced user experience, and drove diamond business growth.

Key Outcomes

B2B Diamond CRM Portal With ERP Synchronisation

Gem is a B2B diamond trading portal with inventory sync to client ERP systems, 4 platforms (web, mobile, backend, cloud), and enterprise security.

Key Outcomes